Insurance industry failures need to be addressed

Submission to NSW Floods Inquiry by Rod Bruem

Executive Summary

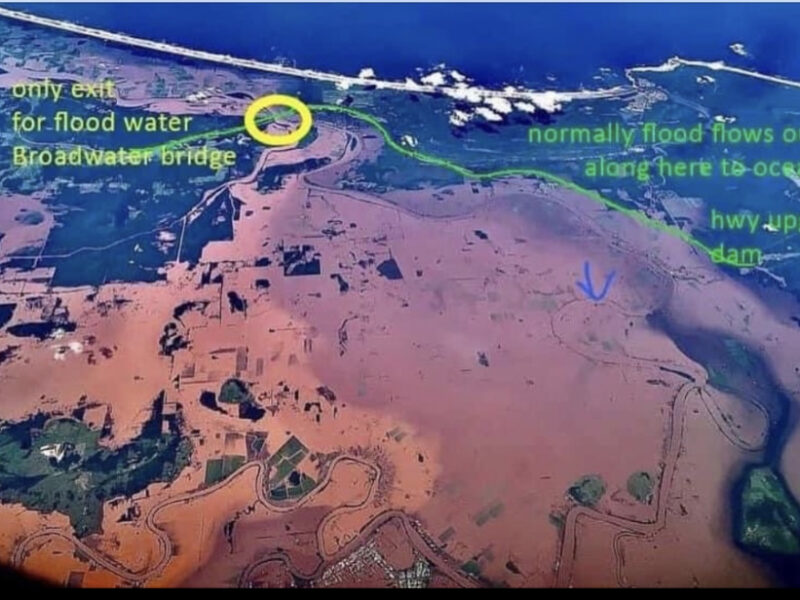

The Lismore/Northern Rivers catastrophic floods of February/March 2022 have demonstrated the Australian general insurance industry is incapable of providing effective protection for businesses and homeowners in the face of extreme and damaging climate events.

This submission proposes that significant government intervention is needed to ensure Australians can invest in homes and businesses knowing they are protected by affordable and effective insurance policies.

The Market Failure

The industry says it expects to pay out some $3.35 billion[i] to cover damages sustained in the floods, however the real cost will be many times higher as businesses and homeowners in the worst-affected areas are not covered for flood damage or are uninsured. The industry either declines to provide flood cover to customers in the high-risk areas, or markets policies at rates that are unaffordable. (It should be noted that some of the worst affected areas also constitute some lowest socio-economic areas of the country[ii].)

This market reality constitutes a failure and has forced the State and Federal Governments to offer direct relief in order to lessen the economic and social impacts of the disaster. NSW taxpayers are bearing the bulk of the costs, with grants of up to $20,000 for homeowners, $50,000 for small businesses and $75,000 for primary producers. The multiple overlapping schemes are complex and difficult to apply. At the time writing, no estimates have been released as to how much the NSW Government expects to pay out. It has been reported few if any of those who’ve sustained significant losses have received any funds[iii]. The delays- and the simple fact people who have lost everything in the floods are unable to provide required documentation, has added to stress, trauma and mental health issues.

Was it a storm, a flood, or a freak catastrophic event?

Some insurers have recognised the flood was a one-in- 600-year catastrophic event and are settling claims. Other companies, including the market leader IAG, are refusing to pay claims unless there is direct evidence of storm damage. Current regulatory arrangements mean it is entirely at the discretion of insurance companies as to how a weather event is categorised and whether to settle a claim or not.

Why NRMA Insurance refuses to pay

A long-time insurance industry executive[iv] says IAG has by far the biggest exposure of any company to the flood disaster and therefore has no choice but to fight every claim put forward.

“Smaller companies with more limited exposure in the Lismore area may decide to simply pay out, because it will save them time and money in the longer term to go forward on that basis. IAG simply can’t afford to do that. They will go through the motions of considering every claim lodged. They will send a hydrologist out to look at each property and document that it was flood damage, just to protect themselves should the customers launch a class action. If there is any evidence of storm damage, signs of water coming through the roof etcetera, they may pay those claims out just to try and save face and minimise their reputational damage. Because they are over-exposed, they have no choice but to play hard ball. For IAG, the bottom-line dictates this is just a flood, not some sort of freak event.”

Evidence from social media[v] shows the process of submitting and going through claims, having the site visit by the hydrologist, only to have the claims ultimately refused has added greatly to the trauma experienced by NRMA Insurance policy holders.

The Northern Australia reinsurance pool

Political leaders in the Northern Rivers have asked for the Federal Government to extend the Northern Australia re-insurance pool to cover northeast NSW[vi], seeing this as a possible solution to the insurance industry market failure. The Commonwealth Government has pledged $10 billion toward the Northern Australia re-insurance pool to make insurance more affordable to some 880,000 homes and businesses north of the Tropic of Capricorn beginning July 1 2022. [vii]

This submission suggests this will not be a workable solution because;

- The insurance industry’s own research shows it falls some 1000 kilometres short of the area likely to be impacted by future tropical storms and floods. [viii] The scheme is limited to areas north of Rockhampton, when climate scientists say cyclone damage will extend to areas as far south as Coffs Harbour.

- The scheme only covers cyclone-related flooding, which would have excluded the recent NSW floods.

- The $10 billion set aside would be multiplied by several times if the scheme was to be extended to include NE NSW and other subtropical parts of the continent.

- There appears to be a lack of support from within the insurance industry. The scheme has yet to be proved.

In summary, it’s a piecemeal or band aid solution designed to appease vocal consumers in marginal North Queensland electorates who’ve been campaigning for more than a decade for help. Climate science indicates a more comprehensive response is needed to help Australians deal with extreme national weather events that can hit anywhere.

The market structure and industry response

Australia’s general insurance business has changed over the past few decades from a time where there were government providers like the GIO in NSW and member-owned mutual providers like the former NRMA. The GIO was established by the NSW Government in the 1920s directly in response to a perceived market failure and a need to protect people. The business was sold off in the 1990s to generate funds to retire state debt.

Today the industry is dominated by private companies which have a fiduciary responsibility to maximise shareholder returns. As has been evidenced in these floods, the need for private companies maximise returns and minimise losses can directly conflict with genuinely caring for customers in their time of need. This conflict only adds to personal suffering experienced following a natural disaster when policy holders wish to quickly rebuild their homes and businesses.

The industry has argued[ix] the best way forward is to minimise the risks primarily by implementing engineering solutions to better protect properties or move them out of harm’s way. While this is a worthy goal, it would take many years to implement and would not help many of those affected by the current market failure.

Conclusion

Insurance is an essential industry directly affecting the prosperity of the country and the health and well-being of its citizens.

It is virtually impossible to conduct business or take out a mortgage unless a property is fully insured. Federal and State Governments have been negligent in their duties to have allowed a situation to develop where thousands of Australians have been left unable to obtain affordable cover.

It is far preferable for policy settings to be in place to allow Australians to protect their property and livelihoods themselves by taking out an insurance policy. It makes sound policy sense for governments to help subsidise a workable insurance system, rather than have taxpayers foot the bill for ineffective and piecemeal handouts in the wake of a natural disaster.

The fact that some insurance companies have recognised the Northern Rivers Floods was a major catastrophe/disaster/1-in-600 year flood event and have agreed to pay out claims, while others are refusing to pay, exposes a regulatory failure that needs to addressed.

Other countries have recognised that governments need to do more, through better consumer regulation and through the establishment of national insurance schemes with taxpayer support.

It is time for Australian governments to stop ignoring this market failure and to act.

About the author

Rod Bruem is a journalist and independent councillor on Ballina Shire Council and Rous County Council. He has interests in a farming business at South Gundurimba on the Wilson River floodplain and an accommodation business in Lismore, both directly impacted by the flood.

He has extensive public policy experience as an advisor to Telstra from 2000 to 2016, taking a leading role in regulatory debates over the privatisation of the corporation and the subsequent establishment of the government-owned National Broadband Network monopoly. He has also served as an advisor to Liberal Party ministers in the Howard, Turnbull and Morrison Governments.

References

[i] [i] https://www.insurancenews.com.au/daily/ica-confirms-recent-flood-is-australias-costliest-at-3-4-billion

[ii] https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/Publications_Archive/CIB/cib9899/99CIB04#4 note ranking of Page electorate

[iv] The author reached out to people via Social media to ask for their advice and experiences. A long-time industry executive spoke to the author on condition of anonymity

[v] See comments on Facebook pages Resilient Lismore and Insurance Fighters Northern Rivers

[vi] https://www.afr.com/politics/mayors-call-for-10b-reinsurance-pool-to-extend-into-northern-nsw-20220331-p5a9nk

[vii] https://www.pm.gov.au/media/morrison-government-deliver-reduced-premiums-through-reinsurance-pool

[viii] NRMA Insurance Wild Weather Tracker Report

[ix] https://insurancecouncil.com.au/wp-content/uploads/2022/02/220222-ICA-Election-Platform-Report.pdf